A known critical element of executive authority involves how power is allocated among the president and administrative agencies. Less appreciated is how the allocation of powers between presidents and the bureaucracy is vital for understanding both coordination and power-sharing that takes place between governmental branches. The Budget and Accounting Act of 1921 (BAA) reforms sought to enhance presidential authority in budgetary matters consistent with Alexander Hamilton’s admonition in Federalist 70 that an ‘energetic executive’ is required for effective governance by providing unity of purpose (i.e., coordination) within the executive, and Hamilton’s equally robust advocacy of competent executive powers that would serve as a check against legislative branch excesses in Federalist 73.

The aim of the BAA reforms was centered on shifting the locus of executive authority from federal agencies to presidents, thereby empowering presidents with the formal authority to both bundle and coordinate agency budgetary proposals into a unified executive budget document. Although the BAA reforms centralized executive budgetary authority under the direct control of presidents, it is widely thought that presidents acquired an institutional advantage at the expense of Congress.

I challenge this commonly held view by proposing that the centralized executive budgetary authority offered by the BAA reforms was mutually beneficial to both the president and Congress. Specifically, these reforms enabled both political branches to attain their shared goal of constraining profligate behavior reflected by executive budget proposals, while also exchanging inter-branch influence over budgetary outcomes predicated on the president’s and Congress’s respective spending priorities. I argue that this power-sharing arrangement attributable to the BAA reforms was made feasible by weakening the budgetary influence of experienced U.S. federal agency heads during the post-reform era. That is, the augmentation of executive authority produced by the BAA reforms did not come at the expense of weakening the legislative branch.

To empirically evaluate these claims, I employ an original historical database covering 37 major U.S. federal agencies between the creation of the Dockery Act of 1894 (FY 1895) that formally structured both budgetary and auditing authority within the Treasury Department and the emergence of large-scale structural changes in the presidential bureaucracy that commenced with the Reorganization Act of 1939 (FY 1940). The advantage of this temporal period is that it limits potential confounding events related to major changes that affected the U.S. federal budgetary process distinct from the BAA reforms.

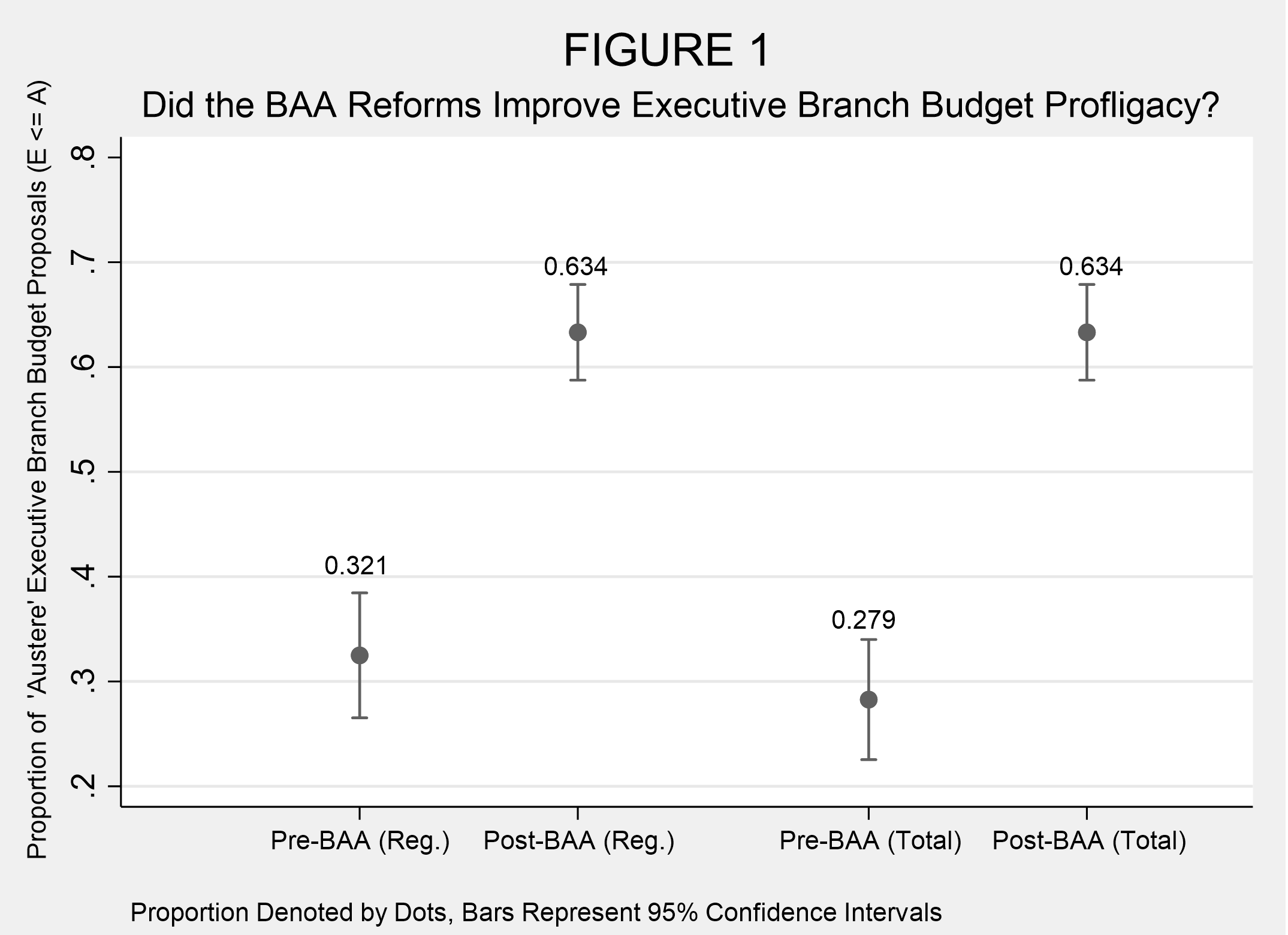

First, I find that centralizing executive budget authority did reduce executive budget profligacy. Figure 1 indicates that the proportion of executive budget proposals that restricted agency funding either at or below congressional appropriations (i.e., austere executive budget proposals) rose sharply in percentage terms from 32.1% and 27.9% respectively for regular and total discretionary budgets under the pre-BAA budgetary system to 63.4% in the post-BAA reform era. This shift reduced the overall constant-dollar spending bias differential for profligate executive budget proposals (E > A) vis-à-vis austere executive budget proposals (E ≤ A) between the pre-BAA reform and post-BAA reform eras in relative terms by 36.91% for regular discretionary budgets and by 65.28% for total discretionary budgets.

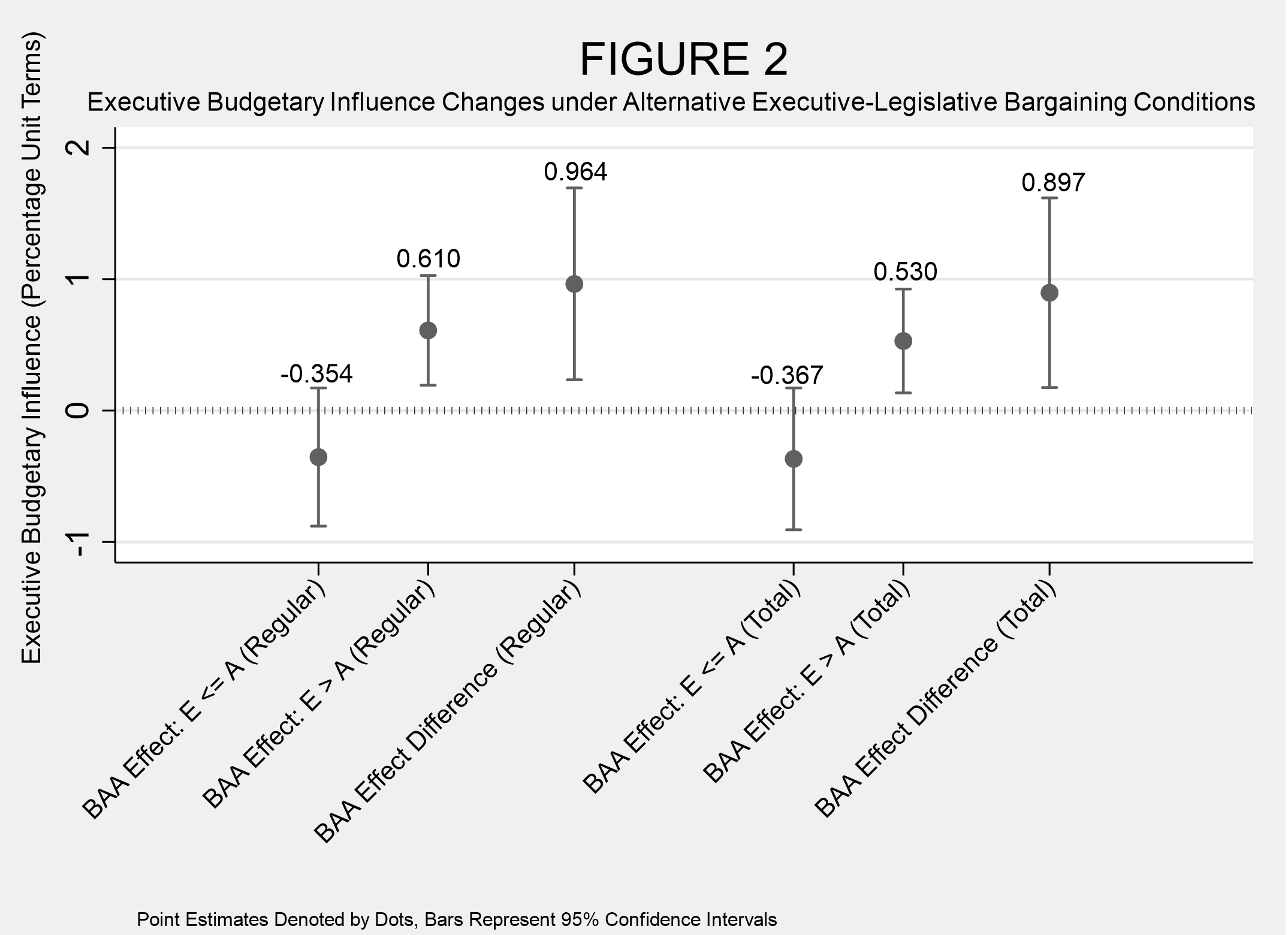

Second, I demonstrate that the BAA reforms triggered a mutually beneficial exchange between the president and Congress’s respective spending priorities. Figure 2 displays that these reforms also enabled presidents to become more successful at shaping budgetary outcomes for those agencies that sought higher funding relative to Congress (profligate executive budget proposals, Eit > Ait) while being less influential when Congress preferred to spend more than the president (austere executive budget proposals, Eit ≤ Ait). The BAA reforms, therefore, created a mutually beneficial shared powers arrangement between the President and Congress that was infeasible under a decentralized budgetary system characterized by diffuse, fragmented executive budgetary powers.

Finally, I evaluate the mechanism that made this mutually beneficial institutional arrangement feasible ― the effectiveness of centralized executive budget authority for constraining the disparate influence of seasoned agency heads who benefitted from establishing robust informal relationships with legislators. Prior to the BAA reforms, an agency head’s experience in office was instrumental for establishing relationships with key legislators, thus shaping the institutional nature of a budgetary process marked by both fragmented and decentralized authority. Prior to the BAA reforms, agency head tenure is shown positively associated with executive budgetary influence for austere executive budget proposals (E ≤ A), and this effect is most pronounced when the agency is seeking extramural funding from Congress. In the post-reform era, however, budgetary outcomes are statistically independent of an agency heads’ level of experience. That is, the variable power of agency heads for shaping budgetary outcomes ceased once presidents were granted centralized control over the executive budgetary process. As a result, post-reform presidents were able to realize mutually beneficial gains for both political branches, while also reducing the overall level of executive budget profligacy.

The broader lesson from this study is a simple, but a powerful one. Executive branch coordination is not only vital for the effective exercise of executive authority, but also for overcoming inter-branch collective action problems within separation of powers systems. Decentralized executive authority premised on diffuse informal relationships is associated with both highly elastic and variable executive policymaking influence. Conversely, centralized executive authority translates into more stable patterns of executive policymaking influence. Put simply, the BAA reforms yielded positive‐sum institutional benefits accrued by both the president and Congress, thus suggesting that fortifying institutional capacity in the American presidency has had positive spillover benefits for enhancing the U.S. Congress’s own institutional capacity.

About the Author

George A. Krause- The University of Georgia

George A. Krause is the Alumni Foundation Distinguished Professor of Public Administration, Department of Public Administration and Policy, The University of Georgia. His primary fields of interest include U.S. executive politics, public administration, political economics, legislative politics, and subnational politics & policymaking. His primary research activities center on understanding (1) organizational behavior, arrangements, and mechanism design both within and across government institutions (public bureaucracies, executive and legislative branches); (2) both the role and distribution of executive authority within U.S. federal and state governments; and (3) decision-making processes in the realm of both mass publics and governments. You can find further information regarding his research here.

George A. Krause is the Alumni Foundation Distinguished Professor of Public Administration, Department of Public Administration and Policy, The University of Georgia. His primary fields of interest include U.S. executive politics, public administration, political economics, legislative politics, and subnational politics & policymaking. His primary research activities center on understanding (1) organizational behavior, arrangements, and mechanism design both within and across government institutions (public bureaucracies, executive and legislative branches); (2) both the role and distribution of executive authority within U.S. federal and state governments; and (3) decision-making processes in the realm of both mass publics and governments. You can find further information regarding his research here.